Don’t Miss Out on the Earned Income Tax Credit

Article Highlights:

- Earned Income Tax Credit (EITC) Qualifications

- Computing the Credit

- Limit on Investment Income

- Military Combat Pay Election

- EITC Scams

- Banning EITC Filers

The Earned Income Tax Credit (EITC) is a tax benefit for working people who have low to moderate income. It provides a tax credit that is treated like tax withholding: it goes to pay an individual’s tax liability, and any excess is paid to the individual in the form of a tax refund.

Qualifications for the credit are based upon the amount of the filer’s earned income, the spouse’s earned income if the filer is married, and the number of qualified children on the tax return. Any child must either be under the age of 19 or be a full-time student under the age of 24 at the end of the year. Low-income earners between the ages of 25 and 64 who don’t have a qualifying child may also qualify.

Earned income generally means income from working, such as W-2 wages and self-employment income.

The credit increases as the taxpayer’s earned income or adjusted gross income (AGI) increases until it reaches a plateau, where it remains constant (at the maximum amount) until it reaches the AGI phase-out threshold. Once the threshold amount is exceeded, the credit is reduced by a set percentage; if income exceeds the top of the phase-out range, no credit is allowed.

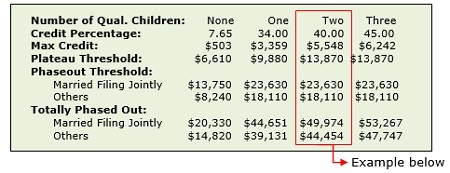

Computing the credit, like all things tax, is complicated, and the credit is actually determined using IRS tables that reflect the dollar amounts at which phaseout begins and ends. However, the illustration below can help approximate the credit for 2015.

Example: A married couple with two children has earned income of $20,000 and a modified AGI of $21,000. If we multiply their earned income by their credit percentage ($20,000 x .40), we come up with $8,000. However, that exceeds the maximum credit of $5,548 for a married couple with two children, so their credit before any phaseout is $5,548. Since their modified AGI is less than the phaseout threshold, then their EITC is $5,548. Had their earned income been $10,000, then their credit would have been $4,000 ($10,000 x .40). If either their earned income or their modified AGI had exceeded $49,974, their EITC would have been totally phased out and they would not have gotten any credit.

There is also a limit on investment income a taxpayer can have and qualify for the EITC. For 2015, that limit is $3,400. Thus if a taxpayer qualifies for EITC but has investment income in excess of $3,400, the taxpayer will not receive any EITC.

Individuals that claim either the foreign earned income or foreign housing exclusion also will not qualify for the earned income credit.

Members of the military can elect to treat all or none of their nontaxable combat pay as earned income for the purposes of computing the EITC. The calculation providing the larger EITC benefit can be used.

Because the potential payout of this credit is so generous, it is the constant target of scammers, and in 2014 the government paid out nearly $18 billion in improper EITC payments. Besides scammers, the qualification for EITC is frequently contested between divorced parents who are both attempting to claim the same child in an effort to qualify for the EITC.

The IRS is authorized to ban taxpayers from claiming the EITC for two years if it determines during an audit that they claimed the credit improperly due to reckless or intentional disregard of the rules. Last year, there were more than 67,000 two-year bans in effect. The ban lasts 10 years if credit was claimed in an earlier year due to fraud.

The government wants those who are entitled to the credit to claim it, and so the IRS widely promotes the credit. However, the rules are quite complex and best addressed by a tax professional.

If you have questions about how the EITC might apply to you, please call this office for additional information. Please understand that a taxpayer who might not normally be required to file a return might still benefit from filing to claim the EITC.

« ABLE Accounts And Individuals With Disabilities | Home | Jointly or Separately? How to File After Saying I Do »

Comments are closed.